Accounting in a Fractured World:

Navigating Geopolitical Disruptions

How global instability is reshaping the finance and accountancy profession

In a world shaped by geopolitical tension…

…sanctions, shifting alliances, and supply chain disruption, finance professionals are being asked to do far more than balance the books. They are expected to navigate uncertainty, strengthen resilience, safeguard integrity, and support strategic decision-making in increasingly volatile conditions.

In this discussion, we explore how global instability is reshaping the finance and accountancy profession, and what leaders must do to remain agile, ethical, and future-ready.

In partnership with AICPA & CIMA

The Association of International Certified Professional Accountants (the Association) advances the reputation, employability, and quality of CPAs, CGMA designation holders, and accounting and financial professionals globally. Founded in 2017 by the AICPA and CIMA, it represents 580,000 AICPA and CIMA members, candidates, and registrants in more than 150 countries and territories, advocating for the public interest and business sustainability on current and emerging issues.

About the Webinar

Geopolitical tensions, trade wars, sanctions, shifting alliances, and supply chain disruptions are creating unprecedented uncertainty for global businesses. Accountants and finance professionals are at the forefront of navigating these risks, ensuring compliance, safeguarding financial integrity, and guiding strategic decisions in an increasingly complex environment.

This webinar explores how geopolitical disruption is influencing the accountancy profession, from reporting and assurance to risk management and strategic advisory. It will equip participants with insight into the risks, responsibilities, and opportunities facing finance professionals in a fractured world.

Key Questions Answered

The Modern Accountability Crisis: Human Agency in an Automated World

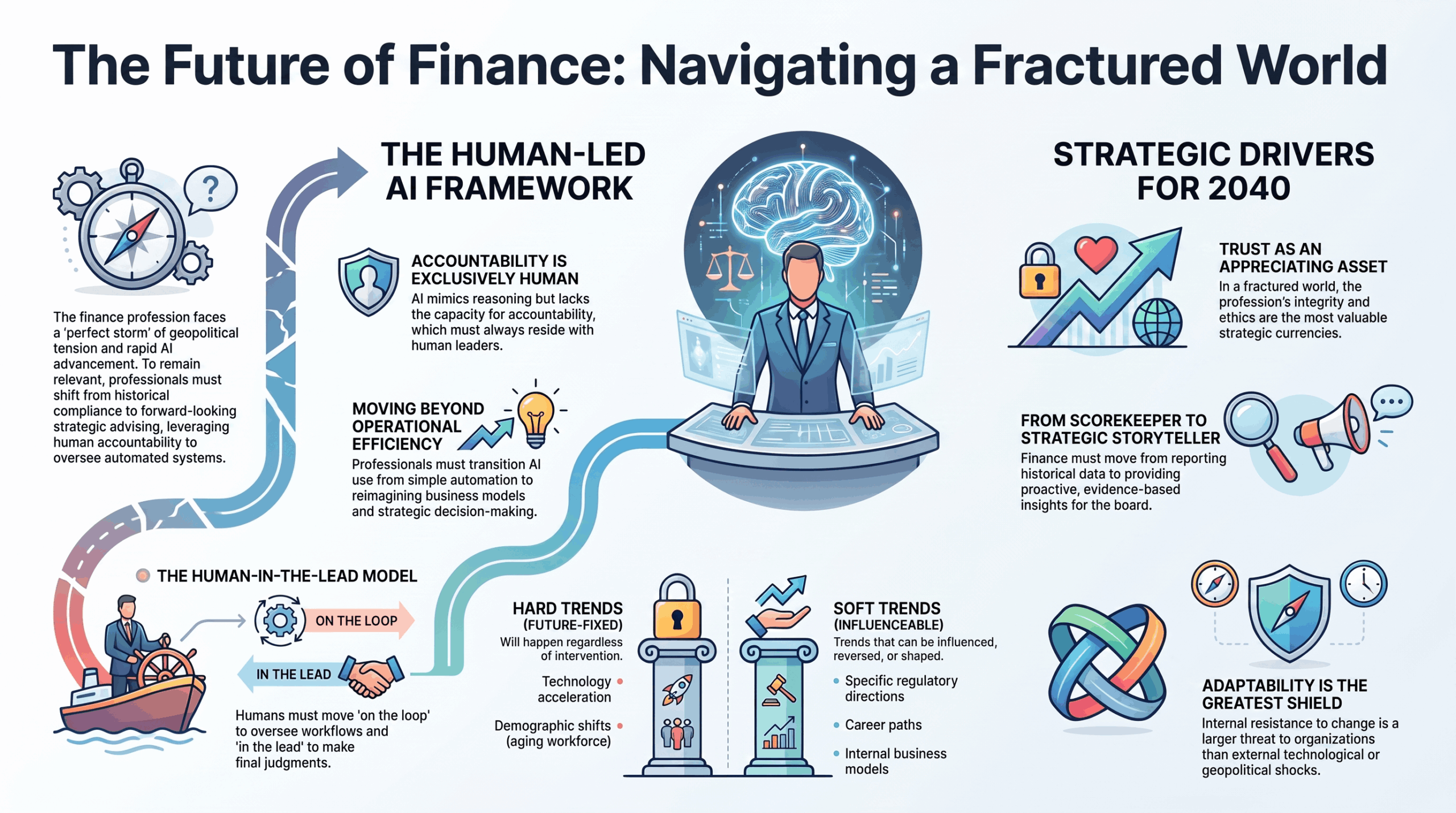

As organizations integrate Artificial Intelligence (AI) into their core operations, the governance landscape is shifting from a “human-in-the-loop” model—where people manage specific automated processes—to a “human-in-the-lead” framework. This is not a mere technicality; it is a critical governance pivot. While 88% of finance professionals are focused on AI’s immediate impact, the board must simultaneously prepare for the “dark horse” of quantum computing. Aware to only 17% of the profession, quantum technology will eventually dwarf AI, offering the potential to process in two minutes what currently takes a millennium. In this hyper-accelerated environment, the Board’s oversight must move beyond technical monitoring to strategic orchestration, ensuring that technology serves organizational values rather than driving blind, automated efficiency.

As AI systems operate across jurisdictions, who holds the ultimate accountability for outcomes and decisions?

Accountability is a non-transferable human asset; the Board must resist the urge to view AI as a governance shortcut. While AI can learn correlations, mimic observed reasoning, and utilize data patterns, it does not “reason” and cannot be held responsible for its outputs. Within the organization, the “buck” stops with the Board, yet the Chief Financial Officer (CFO) serves as the primary “objective conscience” of the business. The CFO maintains the “single source of truth”—the evidence-based data—upon which all strategic judgments rely.

To manage this, leadership must recognize three distinct layers of human involvement:

- Humans In the Loop: Process experts who design and monitor specific automated tasks.

- Humans On the Loop: Cross-functional managers who oversee the workflows and horizontal data flows.

- Humans In the Lead: Decision-makers who exercise ethical judgment and take ultimate accountability.

AI is essentially a “very fast, very accurate, but very stupid employee.” It lacks the ability to handle ambiguity or recognize unethical directives. Without rigorous human leadership, the risks of “hallucinations” and algorithmic bias become existential threats to regulatory compliance.

Key Principle: Governance Competence

Board effectiveness in 2026 depends on a foundational understanding of modern risks—specifically AI governance, quantum disruption, and cross-jurisdictional digital regulations. Relying on 2010-era governance models is a fiduciary failure. The CFO, as the “objective conscience,” must anchor the Board’s duties in hard evidence to counter automated errors.

This human-led accountability is only as effective as the integrity of the information provided. In a fractured world, the “truth” of that information is increasingly the victim of geopolitical pressure.

The Trust Paradox: Professional Integrity Amidst Geopolitical Fractures

In a global environment where geopolitical alliances often overshadow objective truth, trust has become an appreciating asset. Strategic value is no longer found in the mere processing of numbers, but in the ability to provide an ethical foundation that stakeholders can rely on despite shifting political sands.

How does geopolitical fragmentation influence the value and application of professional trust and ethical standards?

Fragmentation complicates ethics by replacing objective facts with “narrative-driven alliances.” While politics leans on ideology, the finance profession must lean on hard evidence. International ethics standards are a unique professional “calling card” that transcends borders, allowing finance leaders to act as trusted advisors regardless of regional tensions.

However, the profession faces an “existential morality crisis.” We see this in jurisdictions like South Africa, where the stakes are life-and-death: professionals who refuse to comply with political narratives or corruption are often “unalived,” while those who surrender their integrity remain employed in entities that deliver unacceptable outcomes. This is the ultimate test of the profession’s purpose.

“People have lost trust in the ability of the profession to serve its original purpose… The biggest threat is when professionals surrender their professional integrity and moral values to assimilate to political narratives and ideology.”

When professionals surrender their values to a political narrative, they become part of the internal rigidity that prevents an organization from responding to objective external shocks.

Adaptation vs. Rigidity: Identifying the True Threat to Organizational Survival

Legacy thinking—applying yesterday’s solutions to today’s problems—is the primary driver of organizational failure. Detecting environmental shifts is insufficient; the capacity to respond without being hampered by internal bureaucracy is what determines survival.

What represents a greater existential threat: external geopolitical shocks or internal resistance to adaptation?

Internal rigidity is a far greater threat than external shocks. Most organizations do not fail because they are blind to change, but because they are too slow to adapt. They lack the “interconnectedness” to understand how a shift in one area—such as new sanctions—cascades into credit and operational risk.

The “Pandemic Playbook” proved that finance functions can be agile through constant scenario planning. However, many organizations committed a strategic failure by reverting to “business as usual” (2019-style thinking) once the crisis subsided. True resilience requires making “crisis-mode” agility a permanent feature of the finance function. To achieve this, leaders must distinguish between:

- Hard Trends (Future-Fixed): Trends that will happen. This includes the massive demographic shift in Africa, which now holds the world’s largest population of under-19s, and the exponential growth of data volumes.

- Soft Trends (Influenceable): Trends that can be changed, such as internal culture, talent strategies, and specific regulatory paths.

Adaptation is impossible without a clear, standardized reporting framework to bridge the gap between divergent global rules.

The Harmonization Debate: Reconciling Divergent Global Standards

There is a permanent strategic tension between regional regulatory sovereignty—such as the EU’s ESG mandates or California’s climate laws—and the corporate need for market efficiency.

Is the vision of globally harmonized accounting and sustainability standards still viable amidst accelerating geopolitical fragmentation?

The path toward harmonization follows a cycle of “divergence then convergence.” We are currently in a period of high divergence, exacerbated by the “tyranny of quarterly reporting,” which often prioritizes short-term political wins over long-term sustainability. However, the long-term driver for convergence is market efficiency; governments eventually seek consistency to attract global investment.

Crucially, the center of gravity is shifting. Leadership in standard-setting is moving away from the West and the EU toward Asia and Southern Africa, where new perspectives on sustainability and integrated reporting are gaining traction.

Current Divergence Trends | Long-term Convergence Drivers |

|---|---|

Regional Sovereignty: EU leading on ESG; US focus on state-level mandates (e.g., California) over SEC federal action. | Market Efficiency: Governments eventually harmonize to reduce the “cost of complexity” and attract capital. |

Geopolitical Alliances: Reporting used as a tool for political advantage or narrative-driven “truth.” | Investor Demand: Global investors require comparable (IFRS-style) data to protect long-term investments. |

Leadership Shift: Traditional Western standard-setting is being challenged by emerging leadership in Asia and Southern Africa. | Standardized Ethics: The universal application of international ethics codes as a foundational global “language.” |

Managing these complex standards requires a new generation of talent who can move beyond the “scorekeeper” role.

The Future of the Profession: Redefining the Finance Career Pipeline

The finance function is evolving from “scorekeepers” (recording history) to “storytellers” (navigating the future). This shift is fundamentally transforming the talent pipeline and the very definition of a finance career.

How will AI reshape the job market and what should new entrants expect regarding career opportunities?

AI is eroding the “traditional apprenticeship model” at the bottom of the pyramid. Entry-level roles involving manual data reconciliation are disappearing. Consequently, new entrants cannot learn the “basics” through manual labor; they must enter the workforce with higher-level cognitive skills already in place.

To survive, the next generation must focus on human capabilities that AI cannot mimic: critical thinking, systems thinking, and ethical reasoning. Because the traditional “learn-on-the-job” model for juniors is broken, education is shifting toward high-fidelity simulations to provide the experience once gained in junior roles.

Action Plan for Future-Proofing Your Career:

- Embrace the “Storyteller” Shift: Move beyond mere compliance to provide proactive, strategic “Navigator” advice to the board.

- Prioritize Systems Thinking: Understand the “why” behind the data and how disparate geopolitical risks interconnect.

- Utilize Simulations: Seek out simulation-based training to replace the lost apprenticeship opportunities at the bottom of the pyramid.

- Commit to Curiosity & Experimentation: Treat professional development as a tool for survival, not a checkbox. Experiment with AI and new tech in controlled environments to understand their limits.

In this fractured and automated world, the choice for the finance professional is binary: embrace these shifts to become a disruptor, or remain rigid and be disrupted.

Short explainer

Podcast-style summary

Alfred Ramosedi, FCMA, CGMA

Alfred Ramosedi is Deputy President of CIMA and a Board Member of the Association of International Certified Professional Accountants. With senior leadership experience across banking and financial services, he has also played a significant role in advancing CIMA’s presence and leadership in Southern Africa.

Andrew Harding, FCMA, CGMA

Andrew Harding leads management accounting activities for the Association of International Certified Professional Accountants, the unified voice of AICPA and CIMA. He is also involved in global reporting and stakeholder advisory initiatives through the IFRS Foundation and the UK Financial Reporting Council.

Alan Johnson

Alan Johnson is Chair of the Good Governance Academy and the immediate past President of IFAC. His international career spans audit, finance, governance, and board leadership, including senior roles at Unilever and other major institutions.

Glossary of key terms

Term | Definition from Source |

|---|---|

AI-Enabled Profession | A professional state where AI is embedded across all workflows, allowing finance experts to move from data processing to proactive, value-added advice. |

Appreciating Asset (Trust) | A concept suggesting that the value of human trust increases as automated and AI-generated information becomes more prevalent. |

Boundary Layer | The second layer of AI deployment where data is connected to provide decision-making intelligence across silos. |

Hard Trends | Future-fixed trends that will definitely happen, such as demographic changes and the continued evolution of technology. |

Humans in the Lead | The decision-making layer of the workforce where specialists use critical thinking and ethical reasoning to take ultimate accountability. |

Objective Conscience | The role of the CFO in providing a neutral, fact-based perspective to the board, ensuring decisions are based on a “single source of truth.” |

Scenario Planning | A forward-looking finance tool used to anticipate various future outcomes, which became critical during the global pandemic. |

Single Source of Truth | The integrated, verified data set managed by finance that serves as the foundation for all strategic and operational decisions. |

Soft Trends | Trends that are not fixed and can be influenced, changed, or reversed through strategic action. |

Storytelling (vs. Scorekeeping) | The shift from simply reporting historical financial numbers to narrating a business’s long-term value, strategy, and sustainability. |