The Accounting Paradox

A Fireside Chat with Jeremy Nicholls

Accounting rarely makes the list when we talk about climate breakdown, inequality, and biodiversity loss, but perhaps it should.

In this thought-provoking fireside chat, accountant, sustainability professional, and activist Jeremy Nicholls explores the ideas behind his new book, The Accounting Paradox, arguing that accounting is not merely a system for reporting economic activity,

it is one of the forces shaping it.

If profit is calculated without accounting for social and environmental harm, are markets rewarding the very behaviours driving today’s global crises?

This compelling conversation on accounting, governance, sustainability, and the possibility of redesigning economic systems to better serve people and planet is inspired by the themes of The Accounting Paradox.

We examine how accounting standards influence investment, define value, and shape the future we are collectively building.

About The Accounting Paradox

In The Accounting Paradox, Jeremy Nicholls argues that financial accounting sits at the heart of today’s ecological, social, and economic challenges. The way accounting standards define profit allows many costs to remain invisible in corporate accounts while being absorbed by society, communities, and the environment.

The book explores how this system shapes capital markets, influences business behaviour, and contributes to rising inequality, biodiversity loss, and climate instability.

Part detective story, part historical exploration, and part manifesto for change, The Accounting Paradox challenges readers to rethink how value is measured — and asks whether repairing accounting itself could help repair the world.

Explainer video

Podcast-style summary

Key questions answered

The global corporate landscape is currently navigating a fundamental pivot from the antiquated doctrine of shareholder primacy toward a model of integrated value creation. This strategic evolution was the focal point of this event, featuring Professor Mervyn King and Jeremy Nicholls.

The dialogue established a stark reality: the current accounting paradigm—long considered the sacrosanct bedrock of business—is facing an existential crisis. As the webinar’s moderator, Carolynn Chalmers, noted, these are not merely technical adjustments for the finance department; they are critical governance issues that demand a structural re-evaluation of how business success is measured.

The following inquiries distill the most critical pivots required for modern business resilience, beginning with the foundational paradox of our economic reality.

What is the "Accounting Paradox," and why does the current definition of "cost" fail modern society?

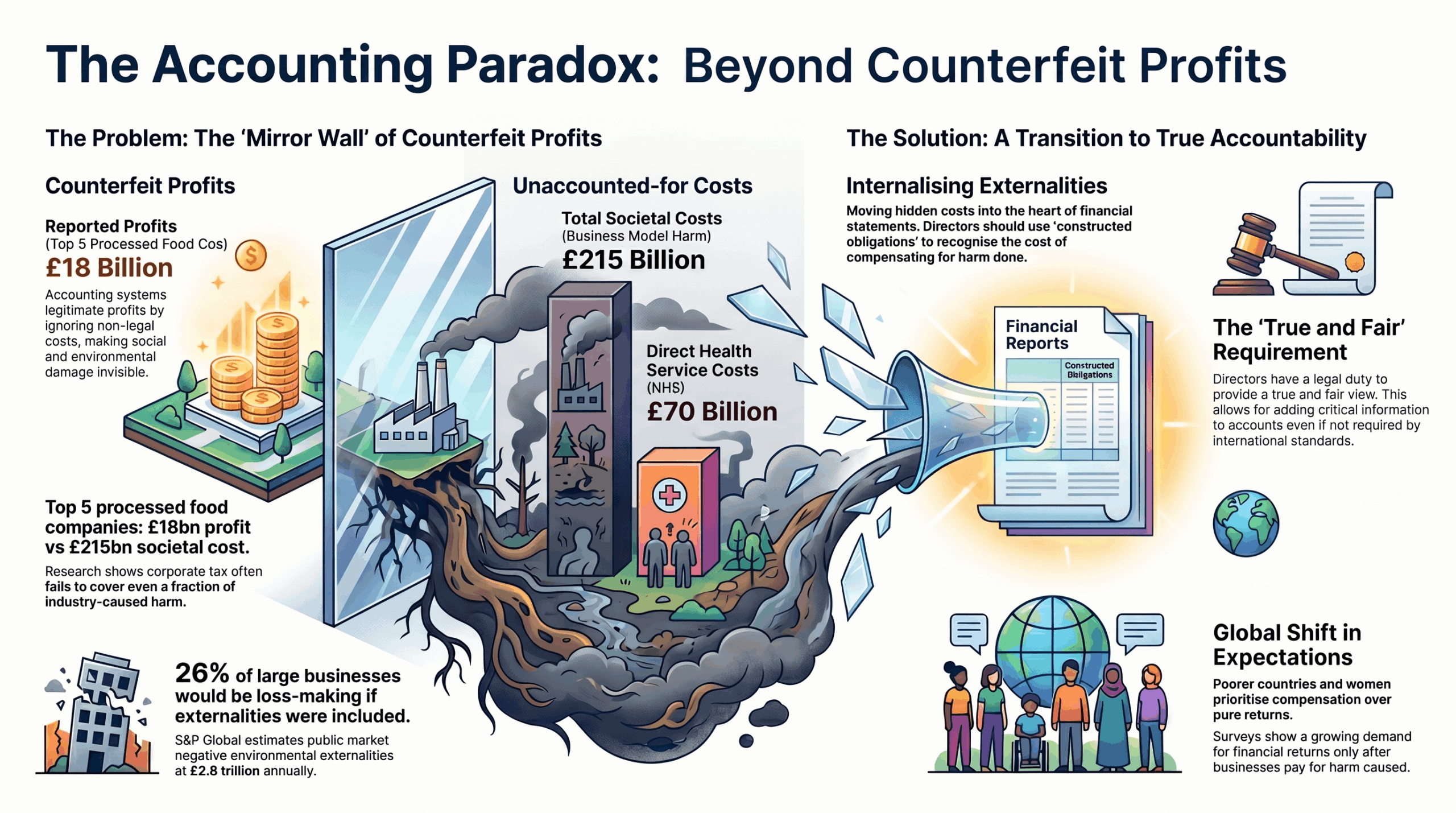

The Accounting Paradox refers to a systemic blind spot: while the global community has spent decades refining sustainability reporting, the foundational “roots” of financial reporting have remained largely untouched. A critical failure of the current paradigm, as identified by Nicholls, is the narrow and exclusionary way we identify cost. In the traditional model, cost is a “brick” used to build a wall between financial performance and societal impact.

The prevailing accounting system prioritizes “legally enforceable costs”—expenditures backed by contracts, invoices, or taxes. However, this narrow focus systematically omits “social costs” or externalities. These are the impacts a business has on the planet and its people that do not yet carry a legal invoice. Because these costs are not legally enforceable, they vanish from the ledger, allowing them to accumulate as systemic risks while companies report healthy, albeit distorted, profits.

Traditional Cost Recognition | Holistic Cost Impact |

|---|---|

Focus: Legally enforceable obligations (contracts, taxes, fines). | Focus: All impacts on people and the planet (externalities). |

Criteria: Based on historical invoices and realized transactions. | Criteria: Based on social/environmental harm and dependency. |

Market Result: “Counterfeit Profits”—financial gains that ignore the depletion of social and natural capital. | Market Result: “True Value Creation”—profits generated after accounting for systemic preservation. |

Systemic Effect: Reinforces the “Mirror Wall,” separating business success from environmental harm. | Systemic Effect: Internalizes costs, providing accurate price signals to the market. |

This restricted definition of cost results in what experts call “counterfeit profits.”

For the strategic investor, this creates a dangerous disconnect. By funding entities that appear profitable only because they ignore externalities, shareholders are unknowingly financing long-term systemic risks. This eventually undermines the future ability of portfolios to generate returns as the external environment becomes too degraded to support viable commerce. Once this wall between profit and harm is identified, we must examine the structural mechanism that maintains this separation.

The accounting system functions as a “Mirror Wall.” To directors, the system acts as a mirror; they see their profits and legal compliance reflected back at them, which effectively prevents them from seeing the actual harm their business models cause. To the public, this wall is “paper-thin”—external observers see both the profits and the mounting environmental costs—but they lack the legal mechanism to link the two.

Accounting has a chilling history of legitimizing business models that society later deemed unacceptable. Nicholls cites 18th-century ledgers where clerks meticulously booked income from the sale of enslaved persons against the transaction costs to calculate a “profit.” This same pattern of legitimizing harm through accounting was repeated with tobacco and asbestos. The accounting system provided the mortar—the “Mirror Wall”—that allowed these models to persist by keeping the harm off the ledger.

Professor Mervyn King highlights the grave risk of the “Circuitous Unaccounted-for Loss.“ When a company causes unaddressed harm to society, such as polluting a city’s water system, it creates a potential cause of action in tort. This liability “circles back” to the company, even if it is not currently on the balance sheet. Directors who allow the Mirror Wall to persist are failing their duty of care. By ignoring these circuitous risks, they are not discharging their duties to the company’s long-term health, leaving the entity vulnerable to future litigation and total value erosion.

If the accounting system is the barrier, then we must scrutinize the effectiveness of our primary regulatory safety net: taxation.

A common corporate defense suggests that “paying taxes” fulfills a company’s social obligation, leaving the government to address any negative externalities. However, the scale of corporate harm often dwarfs tax contributions, rendering this defense strategically bankrupt.

Consider the case study by Professor Tim Jackson regarding the highly processed food industry. The top five companies in this sector reported approximately 23billion in profit,while the societal costs of their business models were estimated at 280 billion, including $90 billion in direct health service costs. Notably, the total corporation tax raised by the entire UK government that year was only $90 billion.

Effectively, the health harm caused by one industry equaled the entire corporation tax take of the nation.

Tax fails as an accountability structure for three primary reasons:

- Disproportionate Scale: Tax is a percentage of profit, but harm is often exponentially larger than the profit itself.

- Temporal Lag: Tax is collected and deployed “after the event,” long after the harm has been caused and often when redress is impossible.

- Lack of Price Signaling: Taxation does not provide investors with granular information to differentiate between sustainable and harmful models at the point of investment.

Alternative historical and cultural models, such as Zakat in Islamic law—where businesses pay 2.5% of net assets toward societal needs—demonstrate that expectations of business can exist beyond simple taxation. Relying on government “redress” is a failed strategy that forces taxpayers to subsidize harmful business models.

The solution requires the professionals with the power to internalize these costs: the accountants.

Professor Mervyn King advocates for the radical evolution of the finance function: the transition from the Chief Financial Officer (CFO) to the Chief Value Officer (CVO). The CVO oversees the integration of the “six capitals”—financial, manufactured, intellectual, human, social and relationship, and natural—ensuring that sustainability is no longer a siloed ESG concern but a core financial reality.

“Financial reporting is critical, but it is not sufficient to discharge the duty of accountability by directors… To put financial and sustainability reporting in two silos is divorced from reality because companies don’t operate on a basis of sustainability issues separate from financial issues.” — Prof. Mervyn King

The “True and Fair” requirement in company law is the most powerful, yet underutilized, tool in the boardroom.

King emphasizes that directors have a duty of accountability that overrides mere compliance with accounting standards. A recent legal opinion on this matter concludes that “directors must exert themselves” to provide a true and fair view. If standard reporting fails to capture significant risks or social costs, the board is legally and ethically obligated to report them. “Integrated Thinking” is now a prerequisite for attracting capital; modern markets increasingly interrogate business models through the three prisms of the economy, society, and the environment.

Shifting a global economic system requires a “Just Transition” to avoid systemic collapse, particularly for the estimated 26% of businesses whose externalities exceed their net income. The transition from the visionary CVO to tactical implementation begins with adding “Notes to the Accounts” that detail the estimated cost of harm compensation, even before these figures are deducted from the final profit.

A gold standard for this transition is the French holding company Kering (parent to Gucci and Saint Laurent), which pioneered the Environmental Profit and Loss (EP&L) account. By making the invisible visible, they have provided a roadmap for internalizing impact.

Strategic Action Guide:

- Directors: Re-evaluate “True and Fair.” Recognize that standards are the floor, not the ceiling. You must exert yourselves to report unaccounted-for costs.

- Investors/Pensioners: Interrogate investment managers. As “universal owners,” pensioners must ask if their funds are invested in models that will be viable in 30 years.

- Governments: Recognize that the accounting system is within your remit to mandate systemic change.

A survey conducted by Social Value International (SVI) and IPSOS reveals a significant reputational risk gap. The data shows a strong correlation between GDP and gender: individuals in lower GDP regions (who experience harm most directly) and women are significantly more likely to prefer financial returns after compensating for harm. This indicates that the public is ahead of regulators, creating a massive risk for multinationals that fail to adapt.

The future of accounting must move from the “Golden Rule” of “He who has the gold makes the rules” to the ethical imperative: “Do unto others as you would have them do unto you.”

By building a system based on empathy and a holistic view of cost, we can create an economy that is sustainable by definition.

About Jeremy Nicholls

Jeremy Nicholls has spent his career challenging how we account for value.

He trained and worked with PwC, including time spent in Liberia and Tanzania, before going on to co-found and lead Social Value International — a global community focused on social accounting and impact measurement. He later contributed to the United Nations Development Programme’s SDG Impact Standards and continues to work across initiatives focused on the relationship between accounting, sustainability, and social value.

Glossary of terms used

Term | Definition |

|---|---|

Accounting Paradox | The contradiction where sustainability is reported separately while the core financial reporting system remains unchanged and ignores systemic harm. |

B Corp | A type of company that changes its articles of association to include a purpose beyond profit, specifically aiming for a “positive material impact” on society and the environment. |

Conceptual Framework | The foundational document that sets out the purpose of accounting, currently prioritizing financial returns for primary users (investors and creditors). |

Constructed Obligation | A non-legal commitment recognized by directors in financial statements to take responsibility for costs or harms caused by the business. |

Counterfeit Profits | A term used by Nicholls’ colleagues to describe profits that appear legitimate under current standards but are only possible because the business has not paid for the harm it caused. |

Externalities | Costs (negative) or benefits (positive) resulting from an economic activity that are experienced by third parties and are not reflected in the cost of goods or services. |

GRI (Global Reporting Initiative) | An international standards organization that helps businesses understand and communicate their impact on issues such as climate change and human rights. |

Integrated Thinking | The active consideration by an organization of the relationships between its various operating and functional units and the capitals it uses or affects. |

ISSB (International Sustainability Standards Board) | A board formed by the IFRS Foundation to develop a global baseline of sustainability disclosure standards (IFRS S1 and IFRS S2) to meet the needs of investors. |

Mirror Wall | The psychological and systemic barrier created by accounting that allows directors to detach the pursuit of profit from the social and environmental costs of their actions. |

Six Capitals | The various resources (Financial, Manufactured, Intellectual, Human, Social/Relationship, and Natural) that organizations use to create value, as defined in the Integrated Reporting framework. |

True and Fair View | A legal requirement in many jurisdictions that financial statements must accurately reflect the economic reality of a company, potentially requiring disclosures beyond standard rules. |

Unaccounted-for Costs | Harms to society or the environment generated by a company that are not traditionally recorded as expenses, effectively subsidizing the company’s reported profit. |

Zakat | An Islamic religious and social obligation where businesses pay 2.5% of net assets to alleviate poverty, serving as a historical example of a non-tax “social expectation.” |